Management of Fixed Assets in a Hungarian Limited Liability Company: Asset Register, Depreciation, Accounting and Tax Rules

Registration, capitalization, depreciation, sale and disposal in manufacturing or asset-intensive businesses

For a company engaged in manufacturing, construction, technical services, logistics or any other asset-intensive activity, the management of machinery, equipment, tools, vehicles and other assets is not a simple accounting formality.

These tools determine the capacity of the company to produce, the quality of its services, the planning of its operation, and the true picture of its financial statements. Therefore, in the case of a limited liability company, the management of tangible assets is an accounting, taxation, financial and operational issue at the same time.

According to the Accounting Act, tangible assets must be recognised as tangible assets that have been put into operation for their intended purpose and that serve the activities of the company permanently, directly or indirectly. This may include, for example, real estate, technical equipment, machinery, vehicles, plant and business equipment, and other equipment.

Why is this especially important for manufacturing or device-intensive companies?

A start-up entrepreneur often thinks “I’ll buy a machine, ask for an invoice for it, and the accountant will take care of it”. However, this is only the beginning of the process.

An existing manufacturing company knows exactly that the real management of assets is much more than that. You need to know when each machine was used, where it is located, who is responsible for it, how much value it has in the books, how quickly it becomes obsolete, whether it needs insurance, when it is due for maintenance, when it should be replaced, and what happens to it if it is sold or scrapped.

A well-managed fixed asset register provides answers to these questions. However, a poorly managed record can cause several problems: inaccurate profit and loss account, incorrect tax base, investments that are difficult to follow, disputed scrapping, missing tools and poor management decision support.

What is considered a tangible asset?

In practice, tangible assets can be, for example:

a CNC machine, press, compressor, production line equipment, measuring instrument, forklift, company vehicle, office equipment, laptop, server, camera, machine tool or even an invested investment in a rented property.

The point is not only that the device exists physically. It is also important that it serves the operation of the business in the long term. For example, in the case of a manufacturing company, a machine can be a direct production tool, while an office computer indirectly supports operation. The Accounting Act also specifically names the machines, equipment, instruments, tools, transport equipment and IT devices that directly serve the activity in the field of technical equipment, machines and vehicles.

Procurement: not all immediate costs

When a company buys a piece of machinery or equipment, it may not immediately appear as a full cost. If the asset serves the company’s activities on a permanent basis, it must typically be registered as a tangible asset, and then its value must be accounted for during the period of use, in the form of depreciation.

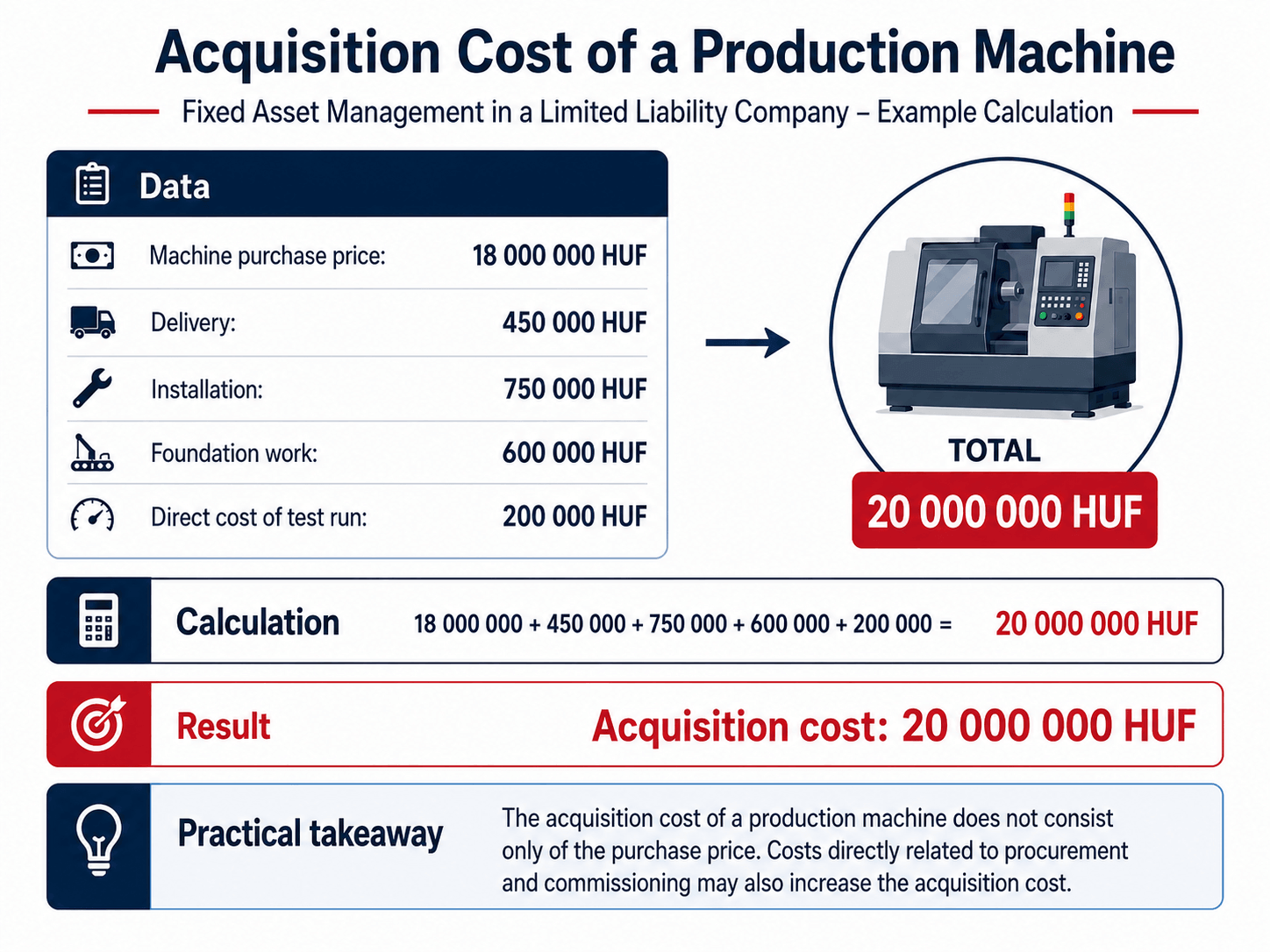

The cost cannot only mean the purchase price on the invoice. The concept of investment includes the acquisition, establishment, production of tangible assets in one’s own enterprise, as well as related activities carried out until commissioning and intended use, such as transport, customs clearance, foundation, commissioning, planning, preparation and implementation.

This is especially important for manufacturing companies. For example, in the case of an imported production machine, it is not enough to see the purchase price of the machine. The total investment cost may include transport, customs, insurance, installation, foundation, expert fees related to the test run and other costs that are directly necessary for the use of the device.

Capitalization: when does the investment become a fixed asset?

The essence of the activation is that the device that was previously registered as an investment will be used for its intended purpose. From this point on, the company actually uses the device in its activities.

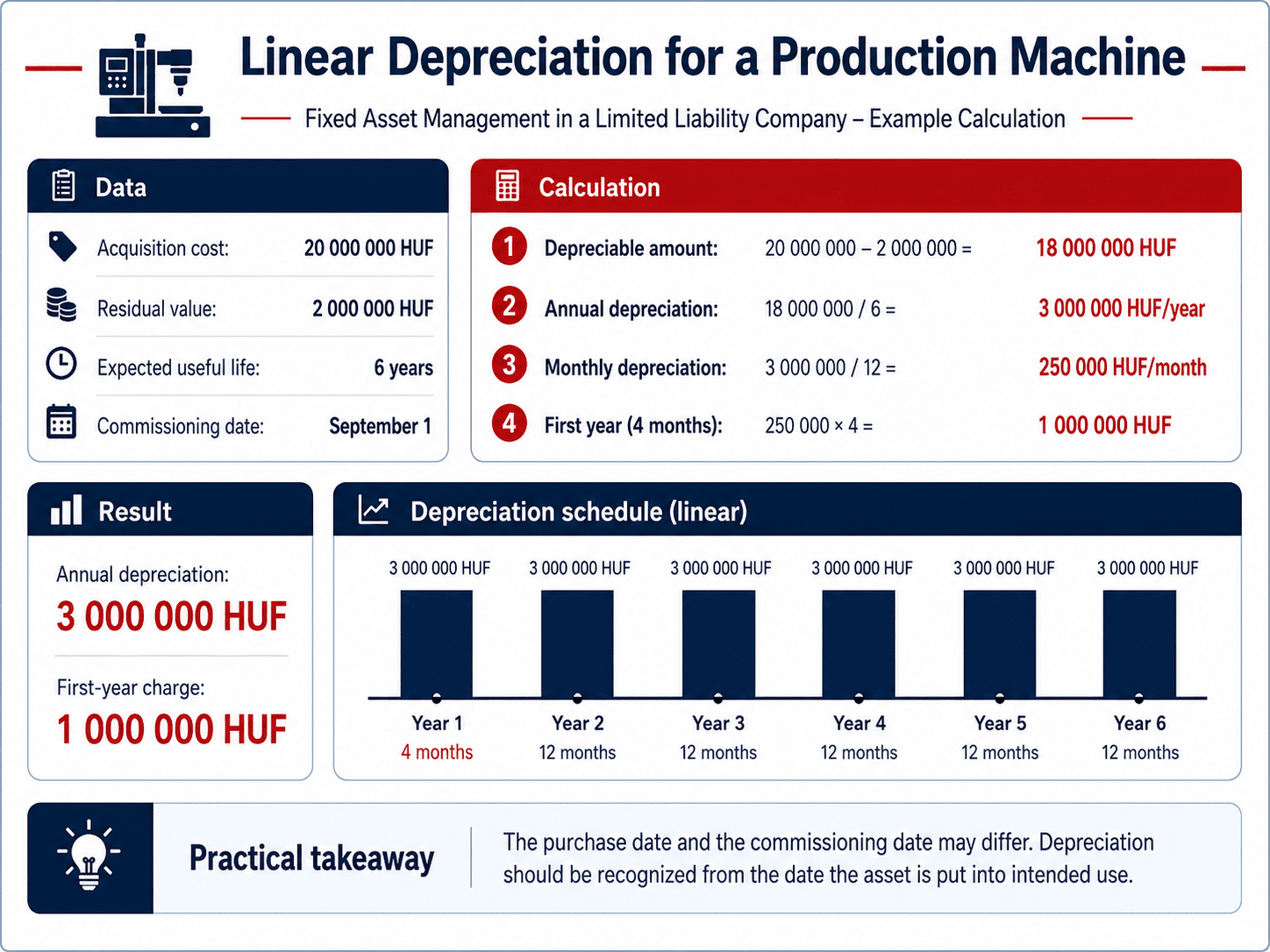

According to the Accounting Act, the date of commissioning is the date when the asset can be used as intended within the framework of the company’s normal activity. This must be credibly documented.

From a practical point of view, it is therefore advisable to prepare a commissioning report at a manufacturing company. This may include the name of the asset, its serial number, its purchase data, location, responsible person, date of use, technical condition, expected useful life, residual value and the depreciation method used.

Depreciation: not just an accounting item, but a business reality

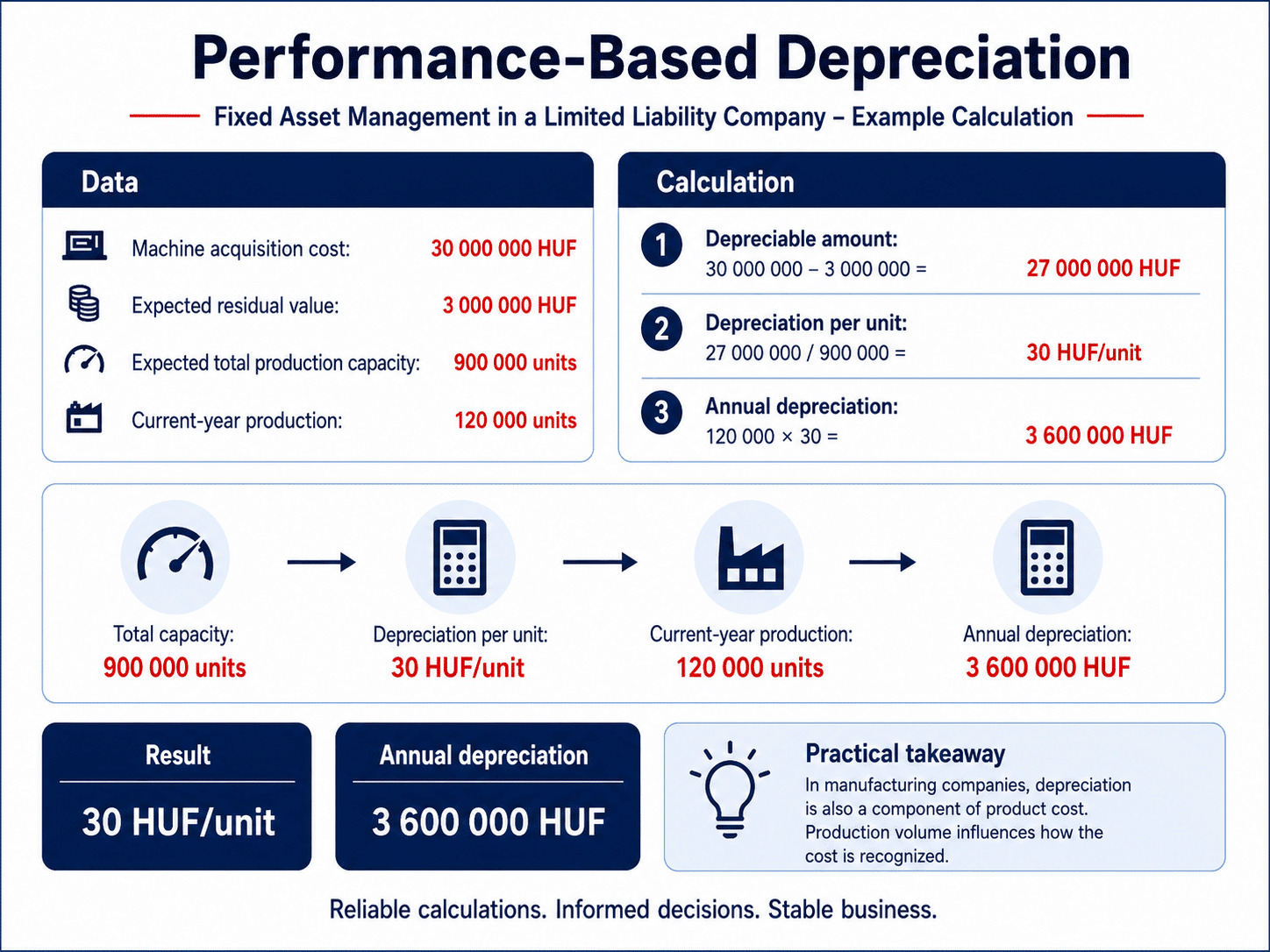

Machinery, equipment and vehicles wear out during use. This is not only a technical issue, but also an accounting issue. According to the Accounting Act, the cost of intangible assets and tangible assets, less the residual value, must be divided into the years in which the assets are expected to be used.

Therefore, a production machine worth HUF 20 million should not usually be treated as if its full value had been used up in a single month. The machine produces for several years, so its cost must also be spread over the period of use.

When planning depreciation, the expected use, lifespan, physical wear and tear, moral obsolescence of the asset and the circumstances of the given business activity must be taken into account. Depreciation must be applied from the date of its intended use, i.e. commissioning.

In the case of a manufacturing company, this means that a different logic may be justified for a production line machine working in three shifts a day than for a less frequently used spare equipment. In the same way, the approach may be different for a rapidly obsolete IT device than for an industrial equipment that can be used in the long term.

Low-value fixed assets

Simpler handling is also possible for devices of lower value. According to the Accounting Act, the cost of rights, intellectual products and tangible assets with an individual acquisition or production value below HUF 200 thousand can be accounted for as a lump sum depreciation at the time of use, depending on the decision of the entrepreneur.

This does not mean that these tools do not need to be dealt with. A manufacturing company can have many tools, measuring devices, hand tools or technical devices of lower value. It is worth following these in internal records, even if they are accounted for in a lump sum from an accounting point of view.

Record-keeping: what to see on a good fixed asset cardboard?

A well-structured fixed asset register is not only useful for the accountant. It is an important decision support tool for the managing director, plant manager, financial manager and owner.

It is advisable to include on a fixed asset cardboard:

- the exact name of the device,

- the unique identifier or serial number,

- the date of purchase, the supplier’s details,

- the cost of the property,

- the date of commissioning,

- the location of the device,

- the responsible person or department,

- the depreciation rate or method used,

- life expectancy,

- the residual value,

- cumulative depreciation,

- the net book value,

- possible renovations, value-adding investments,

- documents for sale, scrapping, or disposal.

Pursuant to the Accounting Act, the opening gross value, increase, decrease and closing gross value, changes in cumulative depreciation and the amount of depreciation for the current year must be presented in the supplementary note to the financial statements, at least broken down by balance sheet item.

Repair, maintenance or renovation?

It is a common question in manufacturing companies whether the work done on a machine is a simple repair, maintenance or renovation to be activated.

Maintenance typically serves to keep the device in working order. This can be, for example, regular oil changes, replacement of wear parts, cleaning, adjustment or minor repairs.

Renovation or value-adding investment, on the other hand, goes beyond normal conservation. If the intervention expands the device, changes its purpose, increases its lifespan or performance, it may also arise as an activation issue. The Accounting Act specifies the cost of uncapitalised works related to expansion, change of purpose, transformation, extension of service life and renovation of tangible assets already in use among investments and renovations.

A practical example: when a worn-out part is replaced on a machine, it is often maintenance or repair. If, on the other hand, the machine is modified to produce at a higher capacity, to produce a new type of product or to significantly extend its service life, then activation may already be considered.

Corporate tax: accounting and tax depreciation are not always the same

The purpose of accounting depreciation is to ensure that the financial statements provide a reliable and fair picture of the company’s assets, financial and income situation. Taxable depreciation, on the other hand, is relevant for determining the corporate tax base.

The Tao. On the basis of the Act, special rules apply to the depreciation that can be applied to the tax base. The law stipulates, among other things, that the depreciation shall be determined in relation to the cost of the asset, and the depreciation recognised as a reduction in the pre-tax profit may not exceed the cost of the asset recognised with the taxpayer.

Therefore, it is important that accounting does not only “book” depreciation, but also manages the accounting and corporate tax consequences together. From the point of view of tax optimization, it is worth taking into account how the asset will appear in the financial statements, how it will affect the result, and what tax base adjustments may arise at the time of purchase.

Asset sales: we don’t just issue an invoice

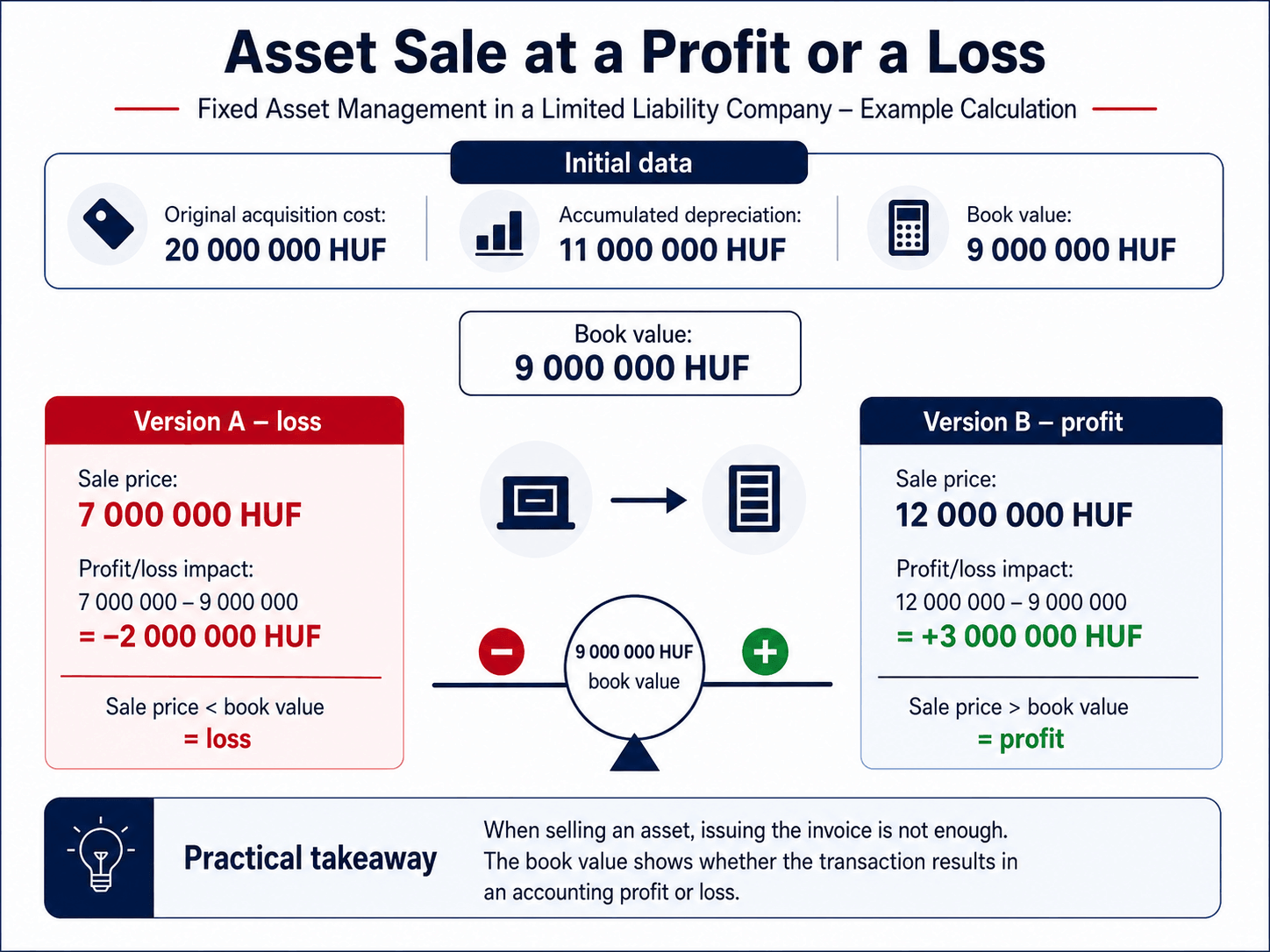

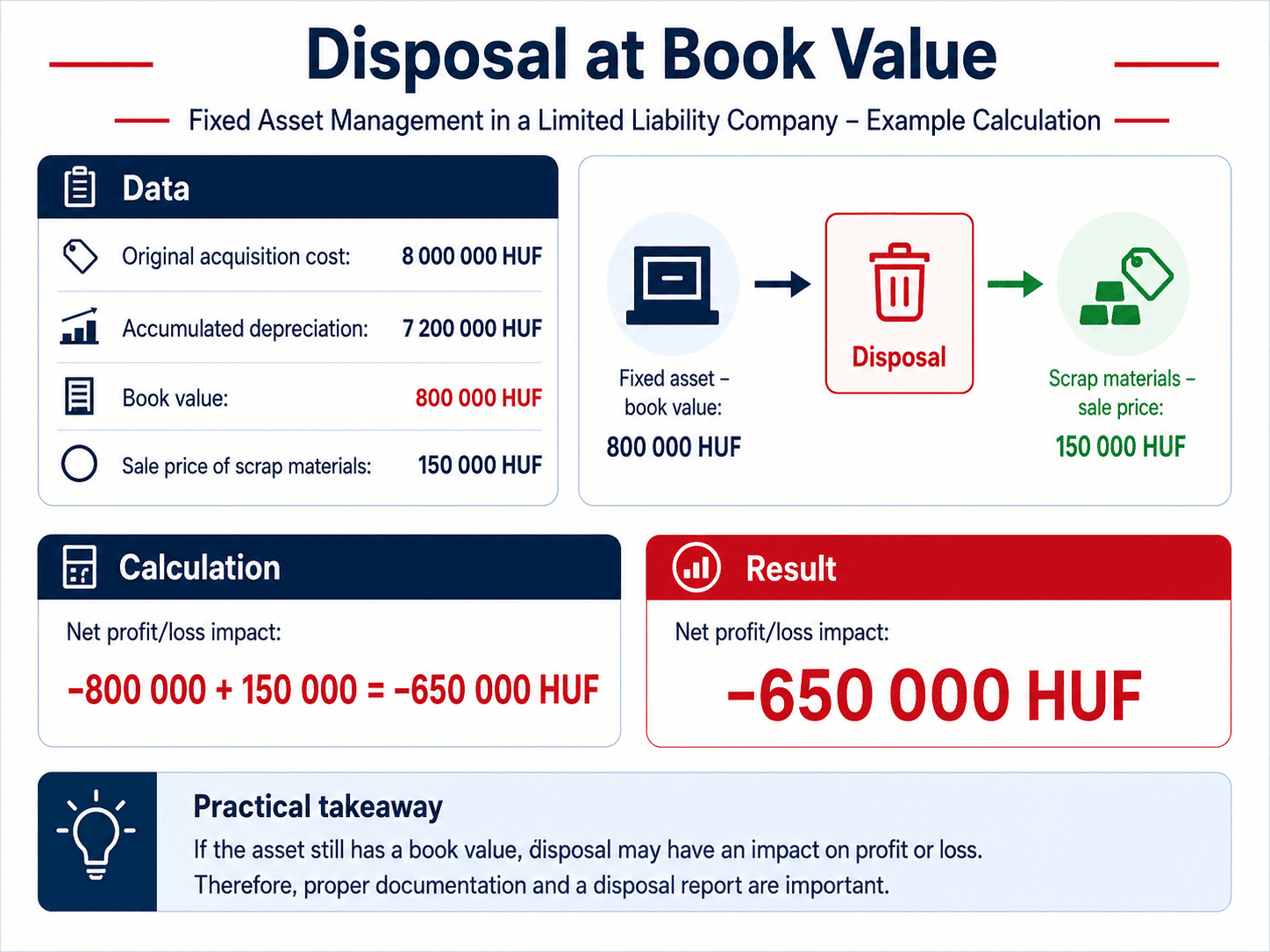

If the company sells a machine, vehicle or equipment, it is not enough to issue a sales invoice. The tangible asset must also be removed from the register.

In this case, the book value of the asset, the depreciation accounted for up to that point, the sales price and the profit and loss effect of the transaction must be determined. The Accounting Act mentions the depreciation of the book value of tangible assets with a quantitative decrease, for example, in the event of sale, transfer free of charge, destruction or deficit.

From a practical point of view, it may be necessary to close the sales contract, invoice, handover document, documentation supporting the market value and the tangible asset cardboard.

Scrapping: when the device is no longer usable or uneconomical

Scrapping does not mean “throwing away the old machine”. This is a documented economic event.

Scrapping can take place if the device is damaged, obsolete, can no longer be repaired economically, is no longer necessary for the company’s activities, or has become technologically unnecessary. In a manufacturing company, this can be common with old tools, custom production equipment, worn-out machines, measuring instruments or IT devices.

According to the Accounting Act, unplanned depreciation must be accounted for if the value of a tangible asset decreases permanently, for example, because it has become redundant, damaged, destroyed, missing or can no longer be used for its intended purpose due to a change in business activity. If the asset is unusable, destroyed or missing, it must be depreciated from fixed assets after the unplanned depreciation has been accounted for.

What should a scrapping report contain?

A good scrapping report includes:

- the name of the instrument,

- Your inventory number or unique identifier,

- the date of purchase and commissioning of the company,

- gross value,

- accumulated depreciation,

- carrying amount,

- the reason for the scrapping,

- a brief description of the technical condition,

- the designation of the person or committee that made the decision,

- the potential value of the utility or waste,

- the manner in which it is destroyed, sold or transported,

- related documents.

In manufacturing companies, it is especially useful if not only the accounting is involved in the scrapping process, but also the plant manager or technical manager. He or she can prove that the given machine or tool is really unusable, technologically obsolete or cannot be repaired economically.

For start-up entrepreneurs: what should you pay attention to before purchasing your first machine?

Before a start-up manufacturer or technical service company buys a larger device, it is worth thinking about a few questions in advance.

- What will the company use the device for?

- How long can I expect to use it?

- Will there be a need for installation, foundation, or trial operation?

- Do I need a special permit, insurance or maintenance contract?

- What costs are associated with commissioning?

- How will the activation be documented?

- Who will be responsible for the device?

- What depreciation logic is justified?

- What happens if the asset is later sold or scrapped?

These questions will not slow down the business. On the contrary, they help to ensure that the company operates in a transparent, controllable and professionally defensible way from the start.

For experienced entrepreneurs: when should you review asset management?

In the case of an already operating company, the revision of the fixed asset register is particularly justified if:

- the machine park has increased significantly,

- a new site or plant has been launched,

- multi-shift production has begun,

- many old tools are still in the books,

- repairs and renovations are frequent,

- tools and gauges are difficult to follow,

- the company is about to invest or take out a loan,

- sale, transformation or voluntary liquidation,

- Management wants a more accurate picture of earnings and cash flow.

In this case, it is not just about “tidying up” accounting. A fixed asset review can help uncover excess capacity, obsolete machinery, unjustified repair costs, and assets that no longer serve the business effectively.

Practical checklist for LLCs

The entire life cycle of a fixed asset should be treated as follows:

Before purchasing: business purpose, cost plan, financing, life expectancy.

At the time of purchase: invoice, contract, delivery and installation documents.

At commissioning: activation report, asset file, responsible person, depreciation plan.

During use: maintenance, repairs, renovations, location change, inventory.

At the end of the year: inventory, valuation, depreciation, examination of possible depreciation beyond the plan.

At the time of sale: invoice, contract, handover, depreciation of book value.

At scrapping: scrapping report, technical justification, handling of useful materials, disposal.

Conclusion

The management of fixed assets is not only the responsibility of the accountant. The managing director of a limited liability company must also understand how machines, equipment, vehicles and other assets are entered in the books, when depreciation can be accounted for, when an investment must be capitalized, how to document commissioning, and what to do in the event of sale or scrapping.

In a manufacturing or asset-intensive business, fixed assets are not just accounting lines. These are the basis of operation, production capacity and in many cases a significant part of the company’s value.

Therefore, well-structured asset management is not an administrative burden, but a business control. It helps you to see costs, capacity, profitability, investment needs, and the real financial situation of your business more accurately.

FirmaX Hungary

Company formation, accounting, tax support and legal advice for businesses in Hungary.

This article is for general informational purposes only. Before making a specific asset purchase, capitalization, scrapping or tax decision, it is worth consulting with an accountant and, if necessary, a tax advisor.